OCTOBER 2025

ASB LOOKS AT

The Compelling Case for Real Estate Investment in Current Environment

Author: Larry Braithwaite, Managing Director, ASB Real Estate Investments

Executive Summary

Real estate markets today face significant uncertainty driven by constrained liquidity, persistent inflation concerns, and volatile fixed income markets. Investors worry about tariff-driven raw material inflation, wage pressures from immigration policy shifts, geopolitical conflicts, and deficit spending that could push Treasury yields and borrowing costs higher. These factors have created widespread hesitation among real estate investors.

But this challenging environment creates an exceptional opportunity. At ASB, we have identified four key factors that suggest upside in today’s market: the historically strong performance of real estate following meaningful pricing corrections, high replacement costs that can offset rate-driven headwinds, real estate’s attractive relative pricing versus other risk assets, and the impact of inflation buttressing higher rents.

Current market conditions mirror the highest-performing real estate vintages in recent history, presenting a compelling case for strategic real estate investment.

Low Liquidity Can Drive Higher Returns

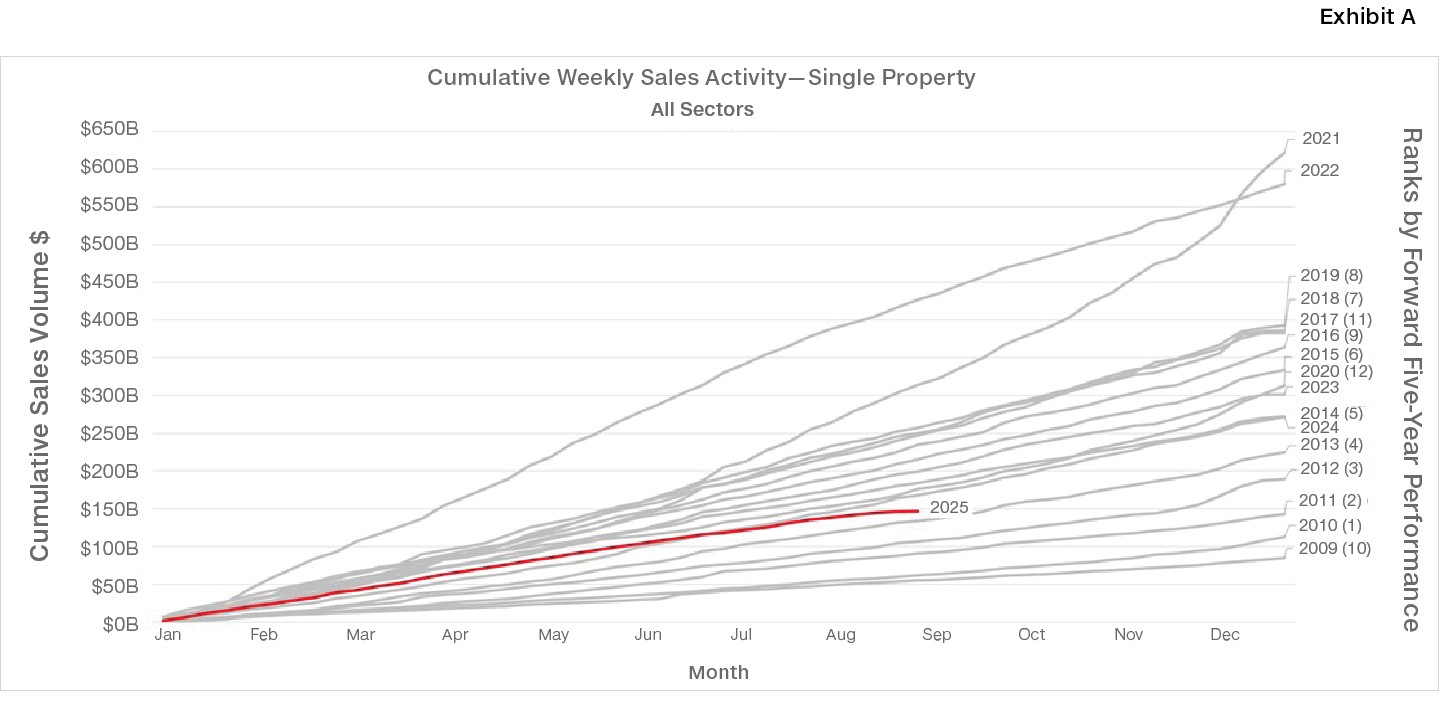

Historically, taking advantage of investor uncertainty and deploying capital at times of market dislocation has generated the best medium-term returns. Exhibit A shows 2025 investment activity YTD alongside other years since 2009. The left-hand vertical axis shows the cumulative real estate sales volume in billions of dollars, and the horizontal axis shows cumulative weeks of the year. The right-hand axis shows the rank of the forward five-year performance for each vintage.

{kind=link}

The current pace of sales is on par with some of the best vintage years for real estate performance. Exhibit B ranks each year by its forward five-year returns, demonstrates a clear pattern where the years with the lowest transaction volumes have consistently produced the highest-performing investment vintages. The only notable exception is 2009, which marked the initial phase of commercial real estate dislocation during which real estate values were written down a cumulative 25%.

{kind=link}

Attractive Basis

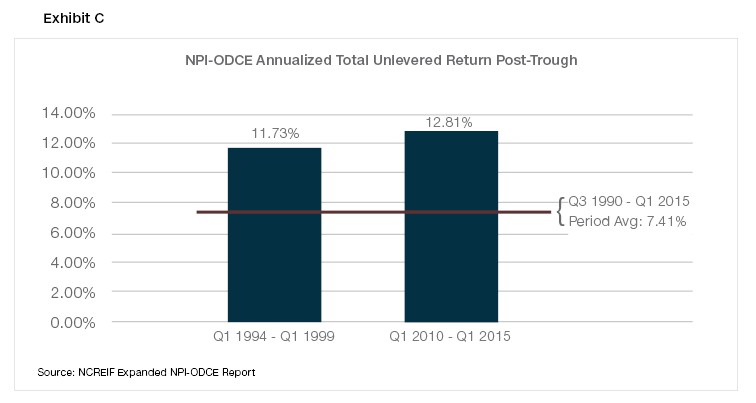

As a result of an inflation-fueled surge in interest rates and real estate investor return requirements, commercial real estate valuations are trading at a 20% weighted average discount to the second half 2022 peak, according to GreenStreet. While it is impossible to rule out the potential for further devaluation, it is important to note that the recent depreciation has many assets valued at a significant discount to replacement cost because while real estate asset values dropped, construction costs increased, further exacerbating the delta between values and replacement cost. Conventional wisdom among real estate investors holds that buying assets below replacement cost represents a prudent entry point which supports future investment performance. Analysis of the past 35 years demonstrates that five-year real estate returns in the wake of a correction of 15% or more significantly outperform the long-term average. Exhibit C shows the five-year returns post peak-to-trough write downs of 16% and 25% in 1993 and 2009 respectively, versus the average return for the period. The current environment presents this exact scenario with quality assets available at discounts, creating compelling entry points for investors.

{kind=link}

Real Estate Pricing: Relative Yields and Other Asset Classes

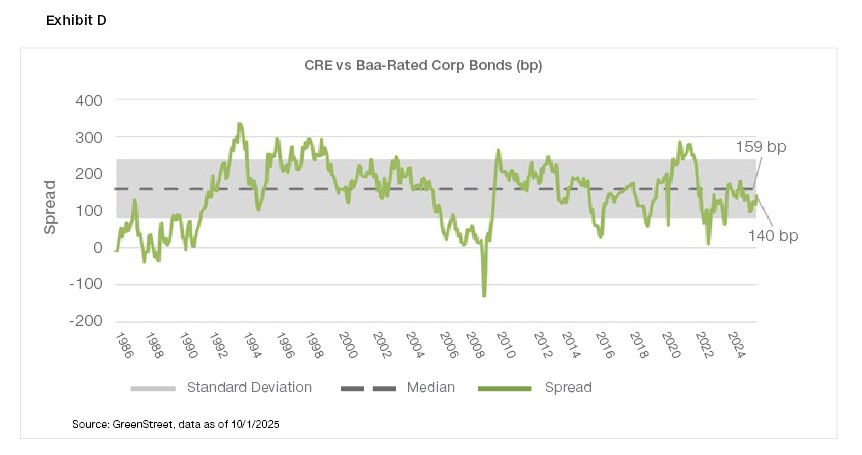

With so many factors impacting Treasuries, some investors prefer to evaluate cap rate spreads to other yield-driven risk assets, such as corporate bonds, to better ascertain relative value. Despite considerable volatility in bond yields, a long-term analysis suggests that cap rate spreads to Baa bonds are only slightly below historical median, suggesting commercial real estate is fairly priced relative to other yield-driven risk assets. This is shown in Exhibit D, where the current spread of 140-basis-points is within a quarter of a standard deviation of the long-term median of 159-basis-points, suggesting that relative pricing for real estate is within the reasonable range of long-term averages.

{kind=link}

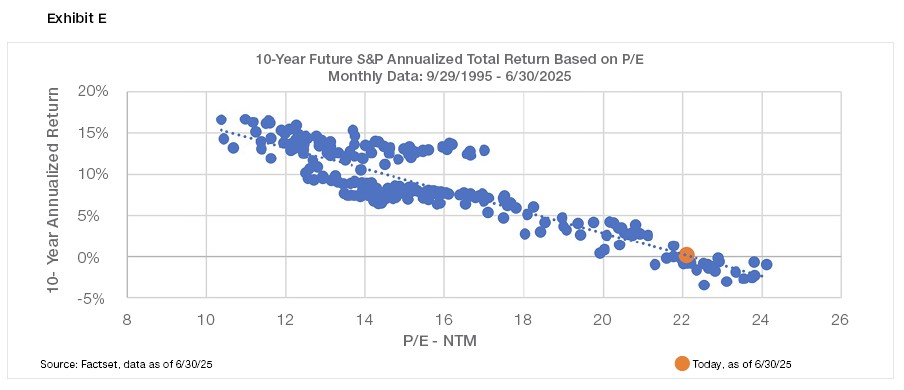

In a wider portfolio, real estate is likely to be included alongside stock market investments as well as bonds and other asset classes. Return expectations for these asset classes are important considerations in determining portfolio allocations. An analysis of the relationship between spot P/E ratios and forward 10-year returns on stocks suggests asymmetric downside for equities (Exhibit E). Historic equity markets where P/E ratios were on par with today’s 22x multiple average flat to negative performance over the next 10 years. This underscores a tough outlook for equities that suggests that real estate offers more attractive risk-adjusted return expectations for the next decade.

{kind=link}

The Trade-Offs of Inflation

As discussed, the inflationary risks that have the potential to push Treasuries, borrowing costs, and cap rates higher, thereby creating downside pricing risk, are important factors to acknowledge. It is equally important to consider the potential positive impact that inflation could have by meaningfully offsetting the negative valuation effect of higher rates. Higher interest rates amid rising raw material and labor costs could cause further disruption to construction starts. In this scenario, the lack of new supply would set the conditions for above-inflation rent growth. New development activity would not ramp up until rents increased to construction-feasible levels, encouraging income-driven appreciation for real estate assets. In this scenario, the direct impact of cost inflation and higher rates could drive factors that have offsetting positive impacts on real estate values.

Summary

The convergence of multiple favorable factors creates an exceptional opportunity:

- Historical Precedent: Vintages during periods of low liquidity have consistently outperformed

- Reduced Competition: Constrained liquidity eliminates many buyers, improving acquisition opportunities

- Attractive Entry Points: Assets trading 20% below recent peaks and below replacement cost

- Relative Value: Superior risk-adjusted returns outlook vs. equities and bonds

- Income Growth Potential: Inflationary environment supports rent appreciation

The confluence of constrained liquidity, attractive valuations, and favorable relative pricing creates a compelling investment thesis that may not persist indefinitely. As market conditions normalize and competition returns, today’s opportunities will disappear.

For investors seeking to capitalize on market dislocation while positioning for long-term wealth creation, core open-end real estate funds offer immediate access to professionally managed portfolios at valuations that reflect current market realities.

Download to view full report and graphics