OCTOBER 5, 2021

Industrial: Outperformance Expected to Continue

The following report is the third in a series from ASB that discusses the outlook for commercial property markets.

Authors:

Larry Braithwaite, Senior Vice President and Portfolio Manager

Cassidy Toth, Head of Research

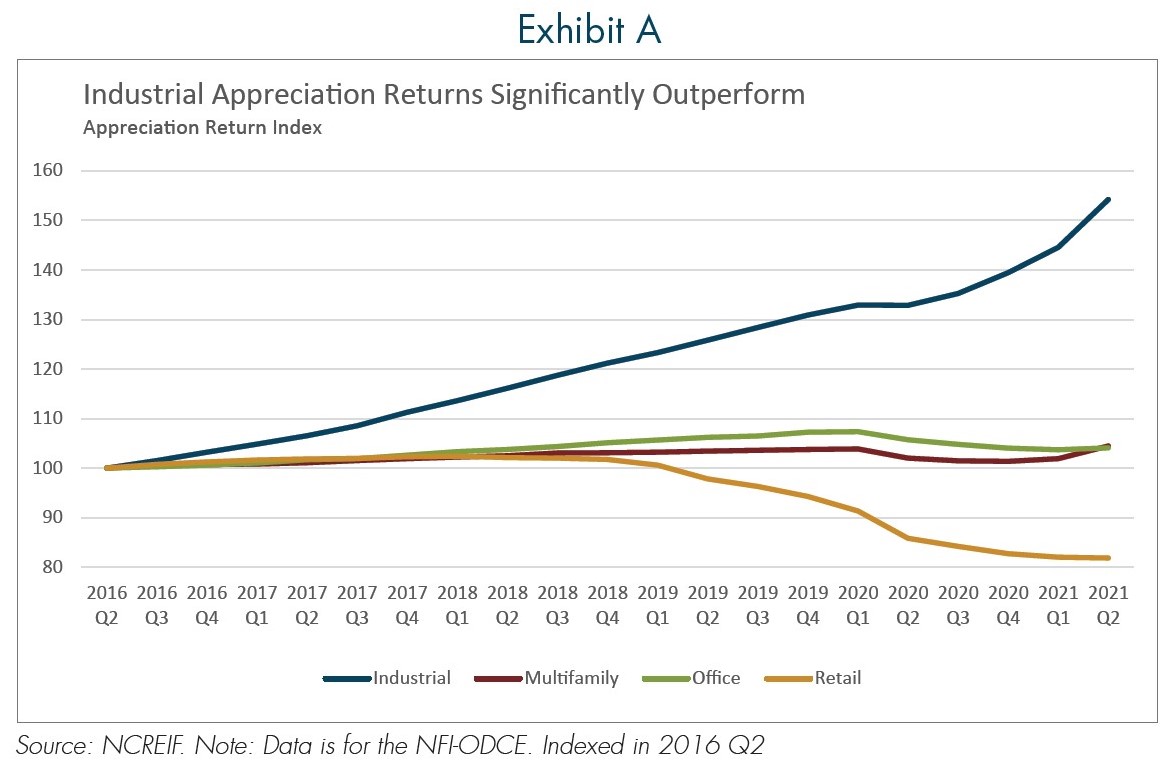

A sharp increase in e-commerce spending during the pandemic and expectations of double-digit growth over the next decade have driven superior investment performance in the white-hot industrial market. E-commerce currently comprises 14.1% of retail sales, up from 10.7% in 2019.1,2 By 2024, e-commerce sales are projected to comprise more than 20% of retail sales, growing to a 30% share by 2030.3 An acceleration in shifting consumer behaviors during the pandemic created spiking demand from e-commerce and third-party logistics users, which require significantly greater warehouse space than brick-and-mortar retail inventory warehousing – representing 80% of logistics tenant leasing demand in 2020 up from 30% in 2014.4 These demand tailwinds have resulted in surging rents and a radical repricing of industrial assets which have appreciated 16% over the past 12 months and 54% over the past five years, significantly outperforming all other major property types and thriving through the pandemic-induced 2020 recession.5 See Exhibit A below.

{kind=link}

Even though port-centric, coastal gateway markets like Northern New Jersey and the Inland Empire have led industrial performance, national trends also are having a broad impact in secondary and tertiary population centers as retailers build out industrial supply chain infrastructure to service valuable pockets of consumer demand. An industrial footprint in proximity to consumers is a critical ingredient in order for e-commerce retailers to accomplish their rapid delivery expectations. It also is a very important factor in managing transportation costs, the greatest expense line item in e-commerce supply chains, ranging from 50% to as much as 70% of total supply-chain costs.6 Today, spiking demand, port delays and labor shortages, all exacerbated by the pandemic are driving above-inflation growth in transportation costs. CBRE reports that container shipping costs from Shanghai have risen by more than 200% year-over-year into critical U.S. ports, including New York/New Jersey and Los Angeles.6

Industrial rents, meanwhile, only comprise 5% of supply chain costs, suggesting users have the incentive to absorb meaningfully higher rents in order to secure mission-critical industrial facilities that help create competitive advantages and specifically lower transportation expenses.7 These factors help explain the surge in industrial rents over the past five years and highlight how landlords can continue to exercise pricing power during the on-going, e-commerce-related industrial expansion.

Currently, tenant demand for smaller last mile assets proximate to high density population centers is especially strong as the number of markets with 20-plus million square feet of tenant requirements has nearly doubled since last year.⁸, Strong industrial growth has been further propelled by new e-commerce entrants, including start-up operators and traditional brick-and-mortar retailers expanding their on-line platforms who are scrambling to preserve market share in an increasingly complex and competitive omni-channel sales environment. As a result, the number of requirements from new e-commerce tenants grew by 21% year-over-year, reinforcing the idea that organic e-commerce demand has the potential to fuel industrial markets for the foreseeable future.8

Another impactful new trend in industrial tenant demand is the shift from “just in time” inventory management to “just in case.” For years, industrial users have streamlined their supply chains in order to boost profitability and drive efficiencies. But, the pandemic exposed the fragility of the “just-in-time” method, prompting logistics experts to pivot to developing more resilient supply chains that can mitigate risk by accommodating surge capacity as well as supplier dislocation. This trend is significantly increasing the need for greater warehousing space to store finished goods, manufacturing parts and components. Further, many U.S. manufacturers who relied on foreign suppliers for components are now turning to U.S. suppliers to reduce the risk of logistics delays in overseas shipping.

Cold Storage: Emerging Subsector. Empty grocery store shelves and soaring food prices during the pandemic made risk mitigation a top priority particularly among food suppliers. This has resulted in increased demand in the cold storage sub-sector comprised of temperature-controlled warehouse space, which facilitates food transfer between farmers and importers, packagers and processors, and ultimately to grocery stores, restaurants and consumers. Further adoption of e-commerce home delivery of groceries is also driving increased demand for cold storage spaces. In 2020, sales volume for cold storage reached a record high of $3.3 billion, up nearly 23% year-over-year.9 Consistent with traditional industrial, cold storage is experiencing strong growth among all sub-segments including import-focused, port-centric facilities, specialized facilities servicing processing plants as well as regional and last-mile distribution facilities meeting consumer demand in primary, secondary and tertiary population centers. Cold storage distribution facilities have specialized operating requirements, deriving revenue from space utilization by the pallet in addition to food handling services, typically on behalf of multiple “sub-tenants.” Such specialization helps serve as a governor on new supply and offers a distinct competitive advantage to landlords who are aligned with the limited number of temperature-controlled warehouse operators in the space. Overall, favorable demand drivers and operating barriers due to specialization combine for an attractive investment context that has spurred robust capital flows into this attractive niche sector.

Next Up: Office

1 U.S. Census Bureau. Estimates Quarterly U.S. Retail Sales (Adjusted) 2Q 2021 Publication. Note: Data is based on trailing-12 months.

2 Insider Intelligence Editors. (2021, June 9). US ecommerce forecast revised upward, 18% growth expected in 2021. https://www.emarketer.com/content/us-ecommerce-forecast-revised-upward-18-growth-expected-2021.

3 Green Street. (2021, March 12). Industrial Sector Update, Full Steam Ahead.

4 CoStar. (2021, June 18). Making Sense of the U.S. Outlook: Pushes and Pulls On CRE.

5 NCREIF. Note: Data is for the NFI-ODCE as of 2021 Q2.

6 CBRE. (2021, September 13). Rising Transportation Costs Help Fuel Record Warehouse Leasing Pace.

7 Prologis. (2021, March 9). Forever Altered: The Future of Logistics Real Estate Demand.

8 JLL. (2021). Industrial Tenant Demand Study.

9 Aaron Jodka. (2021, April 15). The Emergence of Cold Storage. https://knowledge-leader.colliers.com/aaron-jodka/the-emergence-of-cold-storage/

Download to view full report and graphics