NOVEMBER 19, 2021

Rise in Lab Space and Resilience of Medical Office

The following report is the fifth in a series from ASB that discusses the outlook for commercial property markets.

Authors:

Larry Braithwaite, Senior Vice President and Portfolio Manager

Cassidy Toth, Head of Research

The Rise of Lab Space. COVID-19 has highlighted how important the life sciences industry and R&D infrastructure have become to our national security. As a result, public and private funding of pharmaceutical research, development and manufacturing has surged, boosting employment in life sciences and increasing demand for space in lab buildings. Life sciences companies raised over $38 billion in just the first half of 2021, a 77% increase year-over-year, which marks a pronounced acceleration compared to the 18% compound annual growth in life science investment experienced over the past decade.1

The real estate implications of this funding growth have manifested in precipitous growth of lab buildings. These specialized buildings typically feature space that accommodates the handling of biological or chemical agents required in the development of pharmaceutical drugs, including enhanced ventilation infrastructure, significantly greater plumbing requirements, greater loading dock capacity, taller ceiling heights, larger floor plates, enhanced security, and increased power generation. Lab buildings which house R&D facilities often include office space and are widely viewed as a sub-sector of the office market, while lab buildings that manufacture pharmaceuticals, a smaller percentage of the market, are considered an industrial sub-sector. Even though lab space is projected to grow by an aggregate 25% in 2020 and 2021, the hypergrowth market is expected to remain undersupplied.2 During the second quarter of 2021, the three core life sciences markets including Boston, San Francisco Bay area and San Diego averaged leasing activity which comprised an astonishing 17% of inventory.1 Given the strong fundamentals which are expected to continue in the foreseeable future due to strong consumer demand for pharmaceuticals, a healthy capital market for life sciences funding along with an aging population, lab space presents a compelling investment opportunity in the wake of the pandemic. In major life science hubs, strong space demand is driving conversion of office buildings to lab buildings, providing support to office markets and offsetting work from home challenges by reducing traditional office inventory and vacancy.

The Resilience of Medical Office. Another office sub-sector that is garnering significant investor interest is medical office. As the name suggests, medical offices house physician practice space focusing on the patient clinical experience including doctor’s visits, testing and diagnostics, and out-patient procedures. The most prized medical office investments are campus settings that house a critical mass of clinical operations typically on a long-term lease by a major medical institution. In the early stages of the pandemic as lockdowns and strict social distancing measures were announced, many Americans decided to forego elective procedures in order to avoid exposure to medical facilities which were perceived to present elevated risk of COVID-19 infection. Because elective procedures are oftentimes the most lucrative profit centers for medical complexes, payrolls in ambulatory healthcare services, which include medical treatments that do not require hospitalization, lost close to 1.4 million jobs.3 However, the long-term nature of leases helped to insulate fundamentals and a rebound in elective procedures, ambulatory healthcare services payrolls, and medical office utilization have all helped alleviate the acute financial strain that providers experienced during the pandemic.

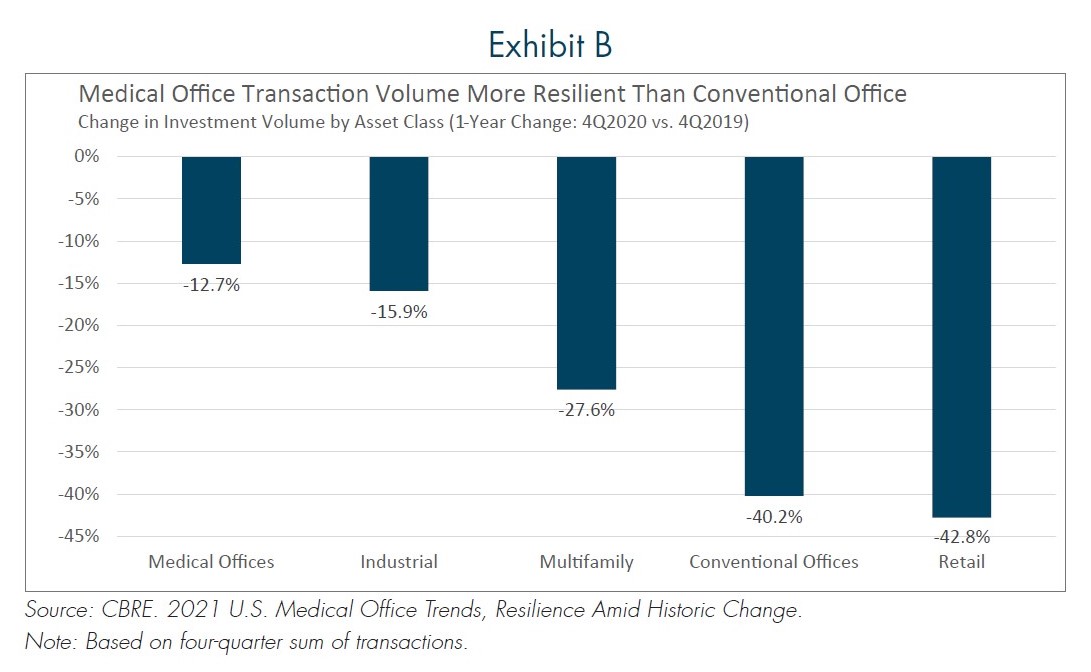

Although COVID may have temporarily dampened demand, the pandemic helped underscore the resilience of medical office space which houses the essential workers who provide essential medical care to the American public. This perspective helped preserve liquidity for medical office which experienced a significantly lower decline in transaction volume compared to traditional office during the pandemic, and even compared favorably to industrial.4 See Exhibit B.

{kind=link}

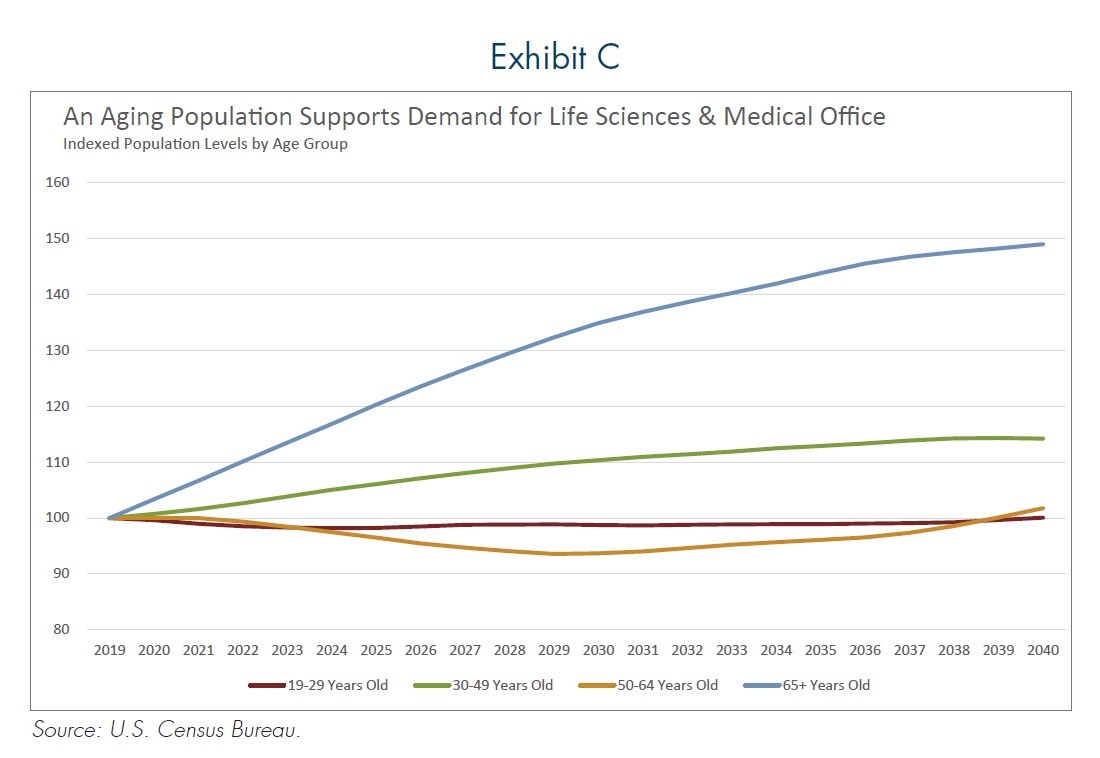

The pandemic appears to have supercharged investor interest in medical office as Marcus & Millichap reports that the number of closings in the six months ending March 2021 represented the strongest six months of deal flow in more than 20 years.5 Looking ahead, the demand for these essential facilities will continue to benefit from the tailwinds of an aging U.S. population that will experience close to a 50% increase in population 65 years and older over the next two decades.6 See Exhibit C.

{kind=link}

1 JLL. (2021). 2021 Life Sciences Real Estate Outlook, The innovation engine is shifting into high gear.

2 ULI & PwC. (2021). 2022 Emerging Trends in Real Estate.

3 U.S. Bureau of Labor Statistics. Data is for the Ambulatory Health Care Services industry measured from Feb.2020 to April 2020.

4 CBRE. (2021). 2021 U.S. Medical Office Trends, Resilience Amid Historic Change.

5 Shaver, Lee. (2021, July 6). Medical Office Draws More Investors Post Pandemic. Read the full article..

6 U.S. Census Bureau. 2017 National Population Projections Datasets.

Download to view full report and graphics