SEPTEMBER 21, 2021

The Strong Rebound in Apartments

The following report is the second in a series from ASB that discusses the outlook for commercial property markets.

Authors:

Larry Braithwaite, Senior Vice President and Portfolio Manager

Cassidy Toth, Head of Research

Just as the pandemic has precipitated dramatically different return outcomes across the major asset classes, divergent results also have occurred across sub-sectors within asset classes, particularly for apartments. Lockdowns, which shut down the nation’s urban centers, eliminated food, beverage, and entertainment amenities and conveniences like short commute times that justified premium rents in the urban core. Renters moved en masse to lower-density and lower-cost suburban locations in secondary and tertiary markets outside of the major gateway submarkets. This movement sharply escalated a trend in the years leading up to the pandemic where many lower cost, lower tax municipalities with strong fiscal health and favorable business climates had experienced stronger growth than major gateway population centers. The sudden outmigration and uptick in urban crime during the pandemic led some market participants to question whether a new cycle of urban decay had begun reminiscent of the 1970’s and 80’s.

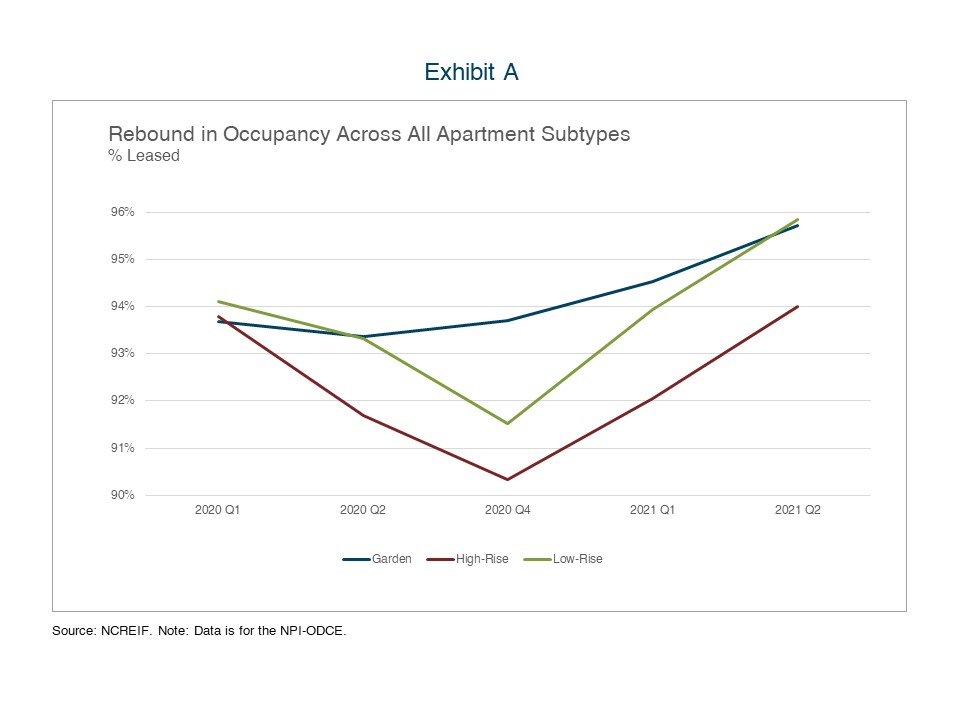

These concerns were largely allayed by late 2020 leading into the first half of 2021 when urban centers experienced strong re-absorption after the rollout of vaccinations, which resulted in relaxed restrictions on restaurants, entertainment venues, and gyms. Young adults who had sought refuge with their parents or adopted nomadic lifestyles taking advantage of remote work options, returned to cities in droves. As a result, high-rise urban apartments experienced a 370-basis-point increase in occupancy to 94% during the first half of 2021, 20 basis points above pre-pandemic levels.1 Other apartment sub-sectors also ended the second quarter with occupancies and rents well above pre-pandemic levels, demonstrating that significant household formation broadly benefited apartment fundamentals. The V-shaped recovery particularly outside of suburban apartments is highlighted in Exhibit Aopens IMAGE file . The strong demand tailwinds combined with a pullback in new multifamily starts during the pandemic suggests that the apartment market is gearing up for a period of elevated NOI growth, bolstering the near-term outlook.

{kind=link}

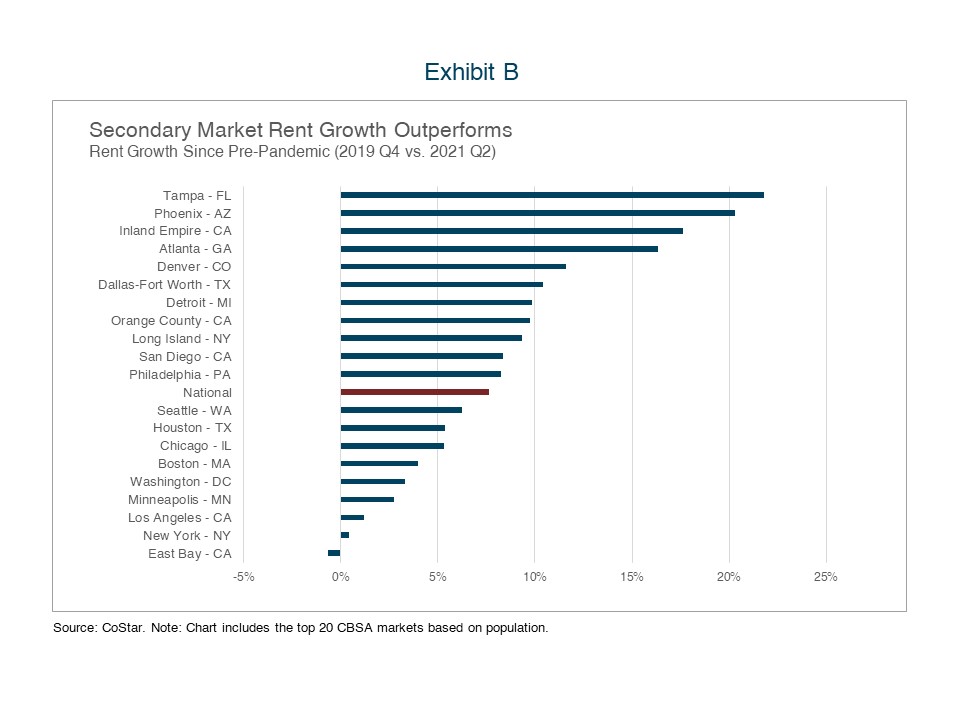

Near-Term Apartments Trends. Although investors are relieved to see a rebound in urban apartment fundamentals, it would be a mistake to believe that the pandemic will not have a lasting impact on the apartment market. Occupancy rates for suburban/garden-style apartments have steadily inched higher throughout the pandemic suggesting that some portion of new suburban demand will be sticky. As millennials burdened with student debt enter their child-rearing years, the primary benefits of suburban living including affordability and more space will remain key demand drivers post-pandemic. In addition, greater acceptance around remote work has accelerated migration to low-cost secondary and tertiary markets. These factors should combine to benefit suburban/garden-style apartment communities in low-cost geographies with strong labor markets. This fact is highlighted when considering the overrepresentation of secondary markets among the top five rent growth markets versus pre-pandemic which include Tampa, Phoenix, Inland Empire, Atlanta and Denver. As shown in Exhibit Bopens IMAGE file , these markets averaged a staggering 17.5% rent growth versus pre-pandemic levels.2

{kind=link}

Single-Family Rentals. The pandemic has also driven increased capital interest in single-family rentals (SFR), located in lower-density, lower-cost geographies. This housing alternative has attracted strong tenant demand by satisfying renters’ space and affordability requirements. As a result, investor interest in the SFR space has been robust. In the first half of 2021, investors made $87 billion in SFR home purchases, and during the second quarter investors accounted for one in every six home purchases in the United States.³ This fast growing interest in the SFR sector is another example of investors taking on slightly higher operating risk in order to achieve exposure to niche sub-sectors with attractive underlying fundamentals.

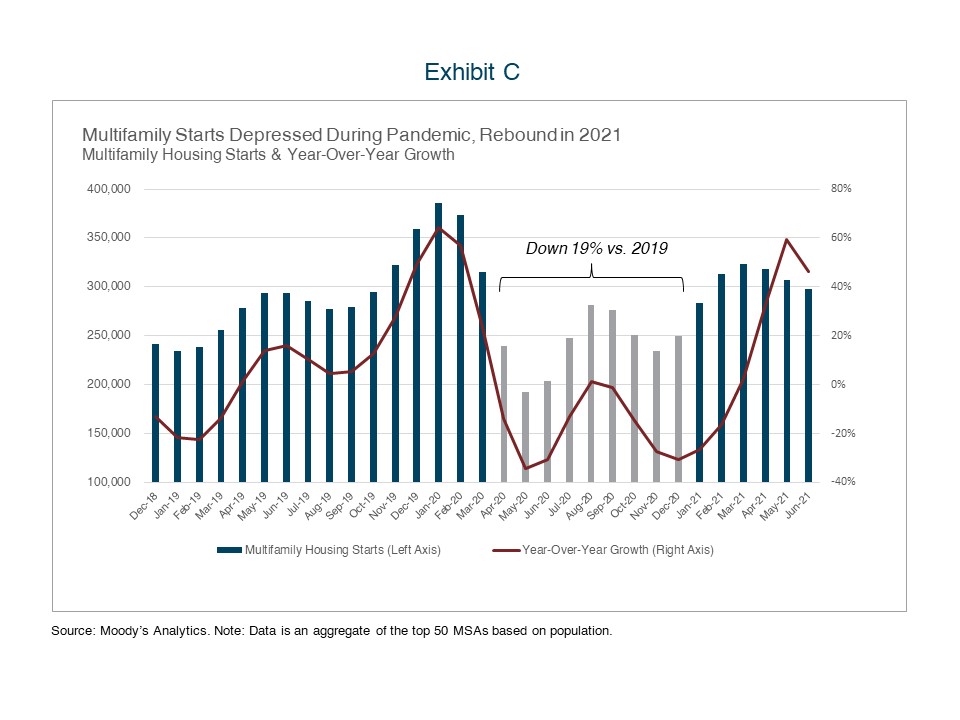

The Apartment Outlook. As occupancies in all apartment categories surge past pre-pandemic levels, continued demand at lower vacancy levels is expected to drive above-inflation rental rate and NOI growth over the near-term. According to CoStar, apartment rents are expected to grow by 6.3% over the next three years, aided in part by a 19% decline in multifamily starts year-over-year from April to December 2020, as shown in Exhibit Copens IMAGE file .4 However, the supply pipeline is building once again as developers respond to strong demand and appreciation. Single-family housing starts are up 29% over 2019 levels in the first half of 2021 as developers race to meet institutional demand for single-family rentals as well as consumer demand for single-family homes.4 At the same time, new starts from multifamily developers in the first half of 2021 are 16% above 2019 levels in response to surging apartment rents.4 Despite new supply, which typically helps reduce pressure on markets, on-going supply chain disruptions resulting in high raw material pricing coupled with acute yield compression due to healthy investor demand for housing means that technical factors are likely to maintain elevated asset pricing and by extension housing costs. Housing costs growing faster than inflation means that consumers are only likely to continue to experience strain in their household budgets. For many, new supply which is naturally concentrated in the higher-rent Class A segment will not moderate their rents. This dynamic reinforces why housing categories like middle-income workforce housing and even manufactured housing, that are affordable and insulated from new supply, are attractive investments over the long-term.

{kind=link}

Next Up: Industrial – Outperformance Expected to Continue

1 NCREIF. Note: Data is for the NFI-ODCE as of 2021 Q2.

2 CoStar. Note: Data is among the largest 20 CBSA markets based on population.

3 Parker, Will. “House Rents Pop Up as New Investors Pile In.” The Wall Street Journal, August 31, 2021, opens in a new windowRead the full article.

4 Moody’s Analytics. Note: Data aggregates starts for the top 50 metropolitan statistical areas based on population.

Download to view full report and graphics