NOVEMBER 11, 2021

The Office Outlook Gains Clarity

The following report is the fourth in a series from ASB that discusses the outlook for commercial property markets.

Authors:

Larry Braithwaite, Senior Vice President and Portfolio Manager

Cassidy Toth, Head of Research

Although the COVID-19 Delta variant has caused more uncertainty about when America’s office utilization will normalize, a consensus has developed in recent months among investors that office buildings will continue to serve as the place where most white-collar work happens despite many employers embracing a hybrid work model. The essential question is whether the inevitable reduction in office space demand due to the rise of work from home will be offset by other factors driving increases in demand.

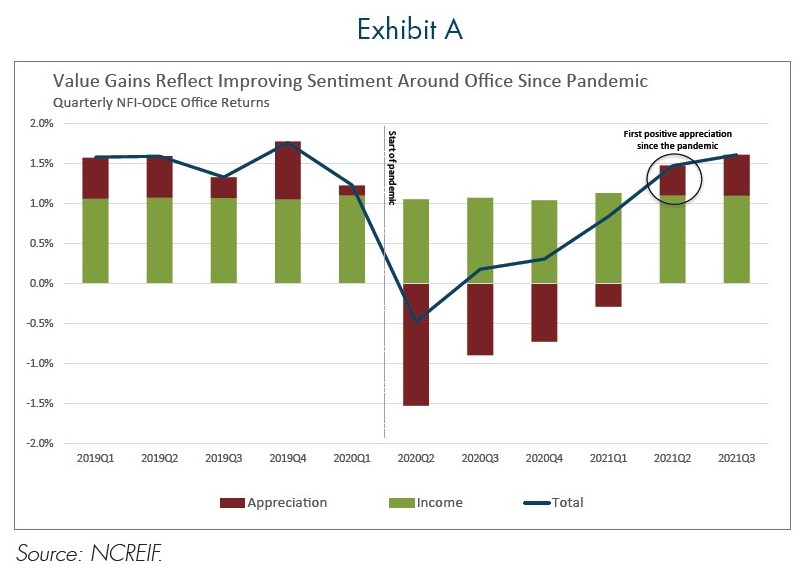

During the depths of the pandemic when offices were closed and companies transitioned to remote work, the viability of the office came into question. Some companies announced permanent work from home plans which further weakened expectations for office demand and resulted in write-downs of office investments. As the pandemic wore on, productivity of remote workers began to slow and logistical challenges of balancing career and family life at home appeared to take a toll on job satisfaction, employee professional development, innovation and workplace culture. As a result, managers dialed back their plans for office space contraction. According to CBRE’s 2021 U.S. Occupier Sentiment Survey, only 9% of large companies plan to significantly shrink office portfolios, down from 39% in the September 2020 survey.1 This somewhat more bullish outlook coupled with increasing vaccination rates and an uptick in office utilization led to office registering positive appreciation in the second quarter 2021 NFI-ODCE for the first time since the start of the pandemic. This trend has continued into the third quarter.2 See Exhibit A.

{kind=link}

The Implications of Hybrid Work. The pandemic demonstrated that many companies can maintain critical business operations via remote footprints. As a result, employees at many companies have pushed for a new normal featuring hybrid-work options. Employers without a partial work-from-home benefit emerging from the pandemic may risk a competitive disadvantage in the labor market. As investors try to quantify the potential impact that the hybrid work model will have on overall office demand and by extension their office investments, they would be well served to develop an understanding of how the priorities of corporate tenants are evolving.

According to a recent CBRE survey, the top objectives that companies are looking to accomplish from their office presence in 2021 are collaboration, culture and engagement.1 Consistent with these objectives, companies reported that wellness, technology, and flexibility account for the top office amenities post-pandemic.1 Although landlords and tenants are still developing a clear understanding of new norms that will characterize the post-pandemic experience, it seems certain that evolving tenant preferences will require additional investment by landlords to satisfy their customers.

The emphasis on collaboration by employers should continue to favor buildings in prime central urban “headquarter” locations with dynamic labor markets, accessible by mass transit and/or in pedestrian friendly districts with dynamic food, beverage, recreation and entertainment amenities. Technology-enabled buildings that prioritize sustainable operations marked by a minimized carbon footprint in addition to wellness and connectedness among tenants will be better equipped to accomplish the environmental, social and governance “ESG” objectives of tenants and investors alike. In addition to evaluating the impact that hybrid work will have on the overall office market, investors will be well served to understand which landlords will be the winners in what promises to be a more competitive office environment.

A decline in office demand is likely given that more than 50% of office tenants generally expect a modest near-term decline in their office footprints.3 However, 93% of survey respondents acknowledge uncertainty and a lack of understanding about how hybrid work will impact future office needs.3 Seemingly opposing survey results underscore this lack of clarity. One of the key factors required to increase efficiency and reduce tenant office footprints is shared workstations. But some data suggests that this solution will not be widely adopted since companies have tested the model in the past and later many have rejected it. A recent survey by global law employment firm Littler Mendelson, found that only 31% of employers are considering an office hoteling model.4 Employers have good reason to approach with caution: a recent study found that hotdesking increased distrust, distractions and uncooperative behavior among Australian employees.5 Greater use of shared workstations is also likely to drive reconfigurations to reduce density and increase functionality of common areas that include additional collaboration zones, phone booths and zoom rooms. The addition of these common area amenities and spacing out workstations potentially offsets the efficiency from the adoption of shared workstations, thereby making the math around the impact on user footprints less straightforward. As a result, outcomes are likely to vary meaningfully, and investors will likely have to wait for clarity because there is no “one size fits all” approach. The dynamics of successful hotdesking adoption can vary across industries and even across departments within the same company.

Organic job growth, excess capacity and sublet overhang are other important factors outside of hotdesking that will impact fundamentals differently across various regions. Certain metros that are poised to experience the strongest gains in office-using job growth, such as Tampa, Orlando, Austin, and Seattle, are likely to see rising tenant demand that more than offsets potential reductions in demand. Gateway markets with strong job growth in technology and life sciences, such as New York and San Francisco, will also see relatively strong office-using job growth in the near-term, despite elevated sublet space that may cause a more protracted rebound. In fact, both San Francisco and New York are starting to see companies remove sub-let space from the market as they recognize the need to accommodate growth. High tax, low growth markets like Cleveland, Philadelphia, Chicago, and Minneapolis are likely to see weaker or negative office demand.

Next Up: Lab Space and Medical Office

1 CBRE. (Spring 2021). The Future of the Office, 2021 U.S. Occupier Sentiment Survey.

2 NCREIF. NFI-ODCE data as of 2021 Q3

3 ULI & PwC. (2021). 2022 Emerging Trends in Real Estate.

4 Littler. (May 2021). The Littler Annual Employer Survey Report.

5 Morrison, R.L., Macky, K.A. (2016). The Demands and Resources Arising from Shared Office Spaces.

Download to view full report and graphics